Award-winning journalist, bestselling author and speaker Eric Weiner noted, “All the golden ages, as we’ve seen in Athens and Hangzhou, contain an element of free for all, a chink in time when the old order has crumbled and a new one is not yet cemented. It’s a jump ball, and that’s when creative genius thrives, when everything is up for grabs.”

Award-winning journalist, bestselling author and speaker Eric Weiner noted, “All the golden ages, as we’ve seen in Athens and Hangzhou, contain an element of free for all, a chink in time when the old order has crumbled and a new one is not yet cemented. It’s a jump ball, and that’s when creative genius thrives, when everything is up for grabs.”

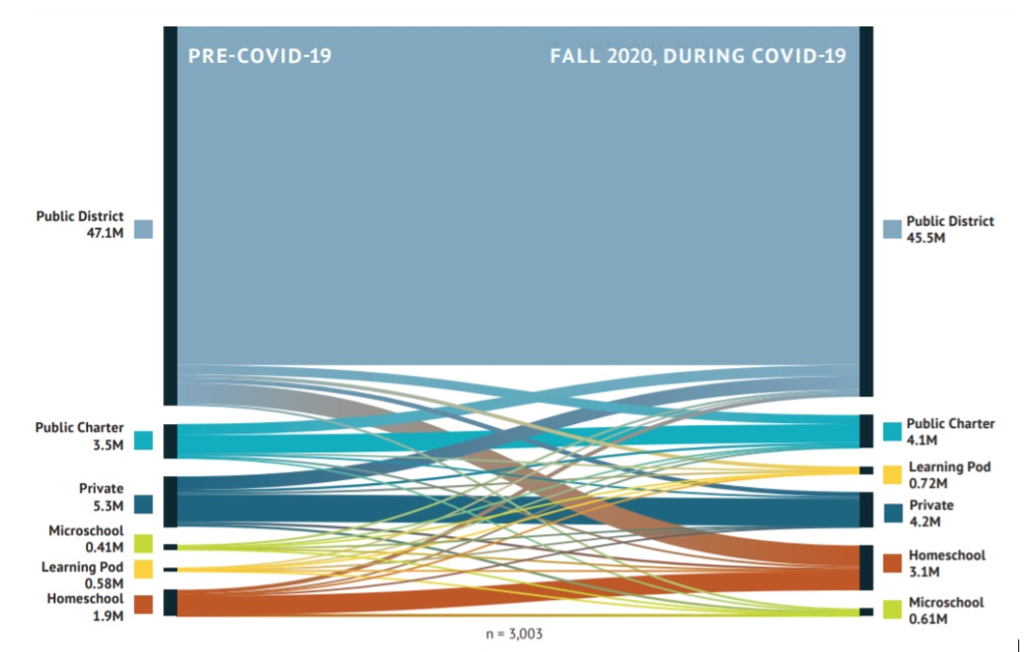

In the chart above from Tyton Partners, a leading investment banking and strategy consulting firm, you see both creative genius and the early stages of a K-12 system that indeed is up for grabs.

Tyton Partners conducted a longitudinal study of K-12 enrollment and family spending, finding interesting trends during the COVID-19 pandemic. Among the initial findings:

· Parents and caregivers took greater responsibility for school decision-making. More than 15% switched their child’s school for the 2020-21 academic year, which is estimated to be 50% higher than behavior pre-pandemic.

· School enrollments shifted with public and private schools experiencing an estimated decrease of 2.6 million in student enrollment; charter schools, homeschooling, learning pods, and micro-schools all realized net increases.

· The pandemic catalyzed growth of supplemental learning pods – defined as cohorts of students gathering in a small group, with adult supervision and outside the framework of their traditional physical or virtual classroom – to learn, explore, and socialize.

· Households spent an estimated $20 billion more on an annualized basis on education-related activities, primarily stemming from the emergence of supplemental learning pods.

· Five activities independently correlated with a parent’s positive perception of his or her child’s learning experience during COVID-19.

· Limited awareness of, and access to, alternative and emerging learning models significantly hindered parent agency, particularly for parents at lower-income levels.

That last point is vitally important, and we will return to it.

According to Tyton Partners’ estimated overall enrollment trends based on schooling decisions of its survey sample, both district schools and private schools lost enrollment from pre-pandemic levels – an estimated 47.1 to 45.6 million public school students; and 5.3 million to 4.2 million private school students.

Every other form of schooling gained enrollment: charter schools (3.5 million to 4.1 million), homeschools (1.9 million to 3.1 million), micro-schools (410,000 to 610,000), and learning pods (580,000 to 720,000).

Additionally, Tyton Partners estimate that almost 7 million students took part in supplemental pods, meaning they remained enrolled in a remote school but participated in an in-person learning pod.

Private schools took the biggest loss in the estimates. The mandatory closures in the spring of 2020, the surge in unemployment, and the uncertainty surrounding the fall of 2021 combined to close many of them. The shape of the post-pandemic world, however, appears much more diverse, with significantly larger charter, home and micro-school sectors.

Many families decided to “red-shirt” their kindergarten-aged students in the fall of 2020 rather than enroll them in “Zoom school.” How these families decide to educate their children will be one of the major shoes to drop in the fall of 2021, with the other being another scramble across sectors. District to homeschool represented the biggest sector jump in the fall of 2020, followed by private to district.

Now back to the equity question raised in that final bullet point.

Micro-schools are schools, and schools require resources to operate. Micro-schools will continue to grow mostly as a form of education that is accessible only to the well-to-do unless lower-income families are able to access their public K-12 funds in education savings accounts.

Some pod operators have been able to access public funding to address equity issues and in a way that empowers families. The battle to empower families continues, as do the possibilities for the empowered.